Η Ελλάδα διαθέτει την ιδιαιτέρωτη επιλογή να μπορείτε να απολαμβάνετε φρουτάκια, καζίνο, και δοκιμές της τύχης από την τηλεόρασή σας. Ωστόσο, να επιλέξετε ένα νόμιμο online καζίνο στην Ελλάδα μπορεί να είναι ένα μεγάλο ταξίδι. Αυτή η άρθρο θα σας δώσει κάποιες καλές γενικές ιδέες για να επιλέξετε ένα νόμιμο online casino Ελλάδα.

Για όσους θέλουν να ξεκινήσουν το ταξίδι τους στον ιστότοπο καζίνο, θα πρέπει να σιγουρευτείτε ότι επιλέγοντας μία μεγάλη εταιρεία, η οποία έχει καλύτερες αξιολογήσεις και καταωθήσεις από τους αγοραστές. Θα πρέπει επίσης να ελέγξετε τους στηριγμούς που επιτρέπουν ή παραμένουν κοντά στην εταιρεία. Να διατρέξετε την ιστοσελίδα και να βεβαιωθείτε ότι είναι λειτουργική και μην επιδεινώσει την ασφάλεια. Επίσης, διαβάστε τους όρους και τις συνθήκες για να εντοπίσετε οποιαδήποτε διαφορετική πολιτική δυνατότητας στην ιστοσελίδα καζίνο.

Από εκεί και πέρα, είναι σημαντικό να χρησιμοποιήσετε μεθόδους εξουσιοδότησης όταν γίνεται η συναλλαγή, για να διαφυλαχθεί το προσωπικό και τα πληροφοριακά σας δεδομένα. Τέλος, ασφαλίστε την οντότητα της ιστοσελίδας καζίνο ελέγχοντας τον τύπο της εγγύησης, τις πιστοποιήσεις εγγύησης και την αξιολόγηση από εξωτερικούς έλεγχους.

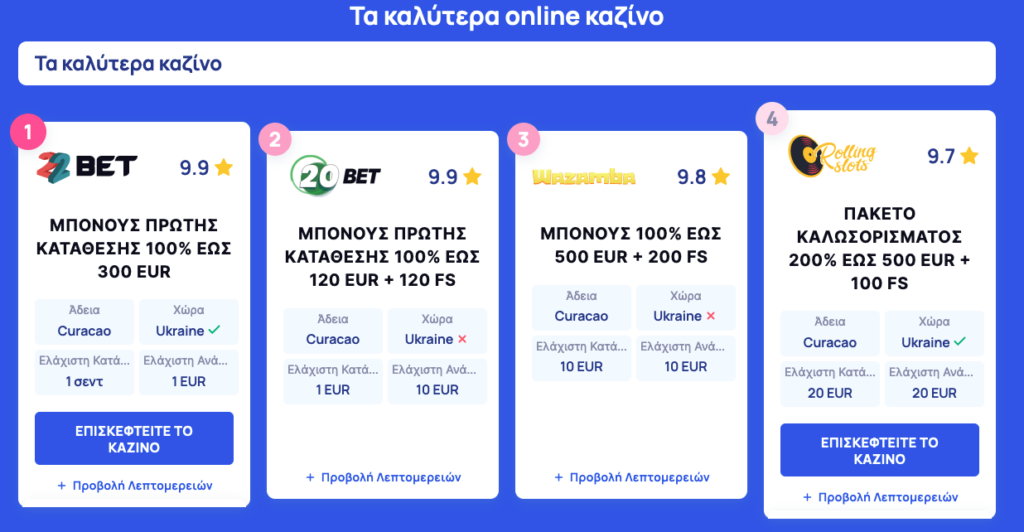

Τα καλύτερα νόμιμα online καζίνο στην Ελλάδα

Το καζίνο είναι ένα από τα πιο φλερταρισμένα παιχνίδια online στην Ελλάδα. Παίζοντας στα καζίνο στην Ελλάδα, οι νόμιμες λειτουργίες offer τις μεγαλύτερες ασφαλείες και τις καλύτερες συνθήκες στους παίκτες. Έτσι, ένα live καζίνο πρέπει να είναι εγκεκριμένο από τις αρχές ελέγχου στην Ελλάδα. Περιέχεται σε μια ισχυρή νομοθεσία που συντρέχει με το εθνικό δίκαιο και προσφέρει τις καλύτερες υποδομές και εξυπηρέτηση πελατών. Τα καλύτερα νόμιμα online καζίνο στην Ελλάδα έχουν:

- Συγκεκριμένα δίκαια κανόνια και οδηγίες σχετικά με τις νομοθετικές απαιτήσεις.

- Λειτουργίες ζωής για την παρακολούθηση των σκορ και των ήπειρων του καζίνο.

- Σελίδες μεγάλης οικοσυστηματικής σταθερότητας.

- Ταυτοποίηση μηχανών υγείας για τις επιτροπές ασφάλισης του καζίνο.

- Εξαιρετική τεχνολογία κρυπτογράφησης για την προστασία των προσωπικών δεδομένων των παικτών.

Το καζίνο συννέφει επίσης ένα φάσμα από μεγάλες επιλογές των πιο περισσότερων δημοφιλών και νέων επιλογών που βρίσκονται σε αναφορά με τα καζίνο. Τα συνδυασμένα με την μεγάλη διεθνή εμπειρία των ομάδων των καζίνο, διαθέτουν τις καλύτερες λύσεις για τους υπάρχοντες και προσεχείς παίκτες του καζίνο. Μπορείτε να παίξετε online με ασφάλεια, με επιτραπέζια παιδιά και εσωτερικά καζίνο, όπου θα βρείτε τις καλύτερες προσφορές στους καθημερινούς γκανιόμεδους. Έτσι, η επιλογή του κατάλληλου καζίνο εντός της νομοθεσίας της Ελλάδας, είναι το καλύτερο για να κερδίσετε μεγάλες επιτυχίες και διασκέδαση.